Zero Tax Living: How to Manage Your 2026 Salary in Qatar & Kuwait

Having spent years navigating the high-rises of Doha and the busy streets of Kuwait City, I’ve seen expats repeat the same expensive mistakes over and over. Moving to the Gulf is easy; staying wealthy is the hard part. In 2026, a tax free salary in Qatar or Kuwait isn’t just a paycheck, it’s a high stakes financial game. While the 0% income tax remains the biggest draw, the hidden lifestyle tax and rising costs in 2026 can eat your savings alive if you aren’t playing smart.

If you are planning to relocate or are already struggling to save, this guide is your no nonsense roadmap to mastering your Qatar financial management guide and navigating the Kuwait salary structure for expats.

1. Qatar vs. Kuwait 2026: Which One Actually Saves You Money?

Is Kuwait actually cheaper than Qatar in 2026? Look, the short answer is: it depends on what you’re willing to sacrifice. While Doha’s rental market has finally stopped bleeding tenants thanks to a massive construction boom in Lusail and Pearl Island Kuwait is a different story altogether. In areas like Salmiya, the expat housing scene is a total battleground. It’s expensive, it’s competitive, and let’s be real those buildings have seen better decades.

The Brutal Truth

- The Qatar Lifestyle Tax: In Doha, you aren’t just paying for an apartment; you’re paying for the View and the vibe. Yes, the high-end dining will absolutely wreck your budget, but you’re living in a city that feels like 2050. The infrastructure is world-class, period.

- The Kuwait Bureaucracy Tax: Kuwait is where you go for the Savings Grind. Your grocery and utility bills will be lower, sure, but the soul crushing paperwork is the real cost. Between strict residency rules and banking hurdles, having Wasata (connections) isn’t just a luxury it’s a survival tool in 2026.

Monthly Budget Breakdown: 2026 Real World Estimates

But wait, the rent isn’t your biggest enemy it’s the ‘Hidden Costs’ I’ve listed in Section 4 that actually drain your account

| Expense Category | Doha, Qatar (Single Pro) | Kuwait City (Single Pro) |

| Rent (The Big One) | $1,400 – $1,900 | $1,100 – $1,500 |

| Food & Groceries | $450 | $380 |

| Power, Water & Fiber | $220 | $130 |

| Daily Commute | $150 | $120 |

| The “Fun” Budget | $400 | $300 |

| Total Monthly Burn | $2,620 – $3,120 | $2,030 – $2,430 |

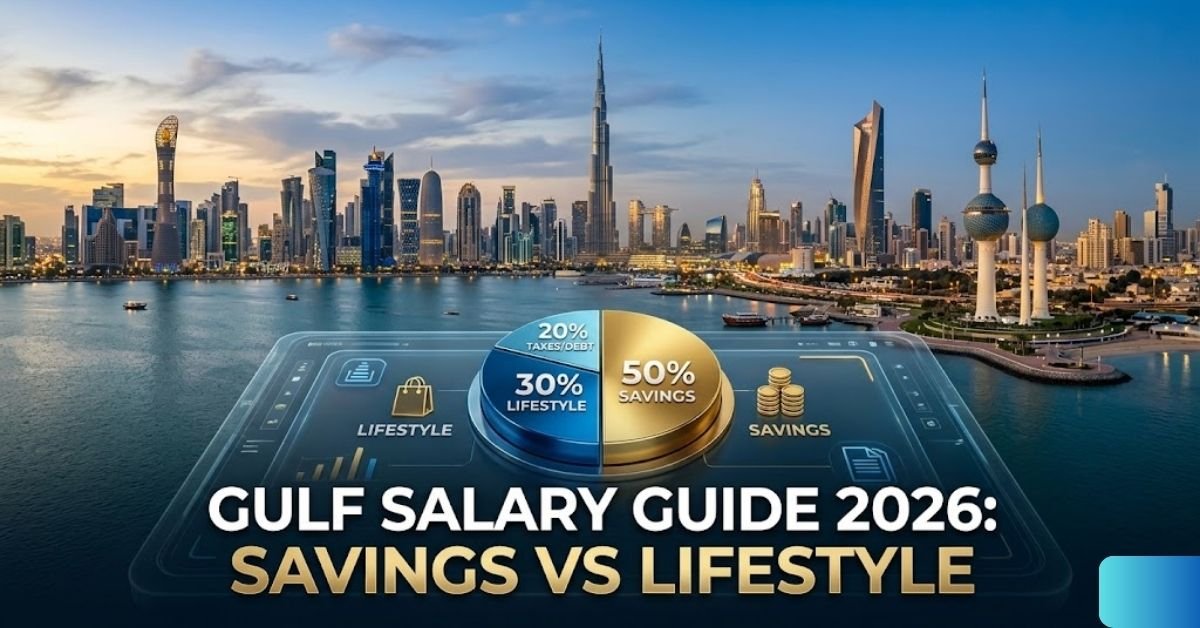

2. Mastering the Zero Tax Mindset: The 50/30/20 Survival Rule

The biggest trap for any new expat? Lifestyle Creep. It starts the moment you see that first $5,000 hit your bank account with zero income tax benefits. Suddenly, that luxury SUV or a spontaneous weekend in the Maldives feels like a necessity rather than a splurge. If you aren’t careful, the Gulf will give you a big salary and take it right back through your own bad habits.

To actually save 50% of your salary in Qatar, you have to trick your own brain. You must treat your savings like a mandatory government tax that you simply cannot avoid. Before you even think about paying your landlord or grabbing that first overpriced coffee:

- Automate Your Wealth (The Set & Forget Strategy): Don’t trust yourself to save at the end of the month. Set up a standing order to move 30% of your paycheck immediately into an offshore banking account or a high-yield savings account in the GCC.

- Create Invisible Money: If that cash isn’t sitting in your main spending account, your brain won’t register it as “available to blow.” Out of sight really is out of mind when it comes to expat wealth.

- Aggressively Audit Your Subscriptions: By 2026, the average expat is bleeding hundreds of dollars on forgotten gym memberships, multiple streaming platforms, and premium VPNs they barely use. Kill them all. If you haven’t used it in 30 days, it’s a parasite on your bank balance.

3. Location Hacks: Where to Live in 2026 to Save Thousands

Where you sign your lease determines your bank balance at the end of the year.

The Qatar Strategy

- Al Wakrah Budget Living: If you work in central Doha, moving to Al Wakrah can save you nearly 25% on rent. With the Gold Line Metro link, the commute is now surgically precise and cost effective.

- Lusail City Utility Bills Warning: Be extremely careful with Lusail. While the buildings are modern, the district cooling charges (Qatar Cool) can be a financial shocker, sometimes hitting $200+ extra per month compared to older parts of Doha where AC is often included.

The Kuwait Strategy

- Salmiya vs. Hawally: In Kuwait, Salmiya offers the prime expat lifestyle, but Hawally provides the savings lifestyle. If your goal is to remit maximum cash home, pick an apartment in Hawally or the outskirts of Farwaniya.

- The Commuter Hack: Living slightly further away in Kuwait can slash rent by 30%, but ensure you have a reliable vehicle, as public transport is not as integrated as Qatar’s Metro system.

4. The 2026 Hidden Costs You Must Factor In

AdSense-safe advice means being honest about the risks. 2026 has brought some shifts that marketing brochures won’t tell you:

GCC VAT & Indirect Taxes

While income tax is 0%, indirect taxes via 2026 GCC VAT updates and “Sin Taxes” on sugary drinks, energy drinks, and tobacco are rising. Your grocery bill in 2026 is roughly 12% higher than it was in 2023.

Expat Health Insurance Costs

Kuwait’s private sector benefits are undergoing a massive overhaul. Ensure your employer provides Comprehensive cover. In 2026, Basic plans often leave you paying 50% co pay for specialist visits or dental work, which can destroy your monthly budget in a single afternoon.

End of Service Gratuity Calculation

Don’t rely on your gratuity for your retirement. It is a Bonus, not a Pension. Use an expat savings plan Middle East specialist to build a real nest egg. Relying on your company’s final payout is a risky 1990s move.

5. Expat Remittance Tips: Don’t Lose Money on the Transfer

Sending money home is where most expats lose 2,3% of their hard-earned cash through Lazy Banking.

- Kill the Bank Transfer: Avoid using traditional banks for international transfers. Digital apps like STC Pay, Ooredoo Money, or Al Ansari Exchange often offer 1% better rates.

- The Decimal Strategy: Track the exchange rate. In 2026, even a small decimal shift in a $2,000 transfer can save you $50–$80. Over a year, that’s $1,000 saved just by being patient with your transfer timing.

6. Strategic Career Moves in 2026

To maximize your Kuwait salary structure, look into niche sectors. In 2026, renewable energy, fintech, and specialized healthcare roles are seeing a 15% salary premium over traditional administrative roles. If you aren’t upskilling, your salary is effectively shrinking due to inflation.

FAQs: The Real Talk Version

Q: Can I really survive on a $2,500 salary in Qatar?

A: Survive? Yes. You’ll live in a shared partition in Mansoura, cook every meal, and use the Metro exclusively. But you won’t be living the dream. For a comfortable expat life with actual savings, $4,000 is the real 2026 baseline.

Q: Which are the best banks for expats in Kuwait?

A: NBK and Gulf Bank are the most expat friendly in 2026 for digital services. However, always check their Minimum Balance requirements. Many expats get hit with $10,$20 monthly fees just for letting their balance drop for a few days.

Q: What are the latest Qatar labor law updates for 2026?

A: The focus is now on Job Mobility. You can switch employers more easily without an NOC, but the process is still paperwork-heavy. Ensure your end of service gratuity is calculated and documented every year, not just at the end of your tenure.

The Final Verdict for 2026

Zero tax living is a double edged sword. It can either be the launchpad for your financial freedom or a cycle of all-spend, no-save regret. The secret is simple: Live like you are still being taxed at 30%, and invest that 30% yourself.

Disclaimer:

This 2026 Gulf relocation guide is purely for sharing information and shouldn’t be taken as official financial or legal advice. Since rental trends and labor laws in Qatar and Kuwait change overnight, you’ll need to double check every cost on official government portals before making any big life moves. I don’t take responsibility for your individual financial choices or any contract issues you might face.